While currently the economic woes in the US seem to be worse than in the EU, the IMF predicts that among developed nations, UK will be the worst hit with a contraction of 2.8% in 2009. The EU overall will shrink by 2%. The US will shrink by a "mere" 1.6% - that's roughly $220 BN reduction in the US GDP. Moreover, the IMF has warned that the UK is so structurally unsound that it will remain in debt for 20 years.

Of course, all this pales in comparison to Iceland. Iceland has become the first Western nation to get IMF help since 1976. With 17.1% inflation and outstanding bank debt that is six times its GDP, Iceland is expected to see 9.6% contraction in its GDP in 2009 and at best no growth in 2010. Their Prime Minister has now been forced to resign. Here's a summary of the timeline of key events in Iceland.

Meanwhile, while many developing economies have been ravaged by a combination of the drop in demand from Western economies and the drop in oil prices (a mixed blessing, depending on where you are), they are expected to continue to grow, although their growth will slow substantially.

Wednesday, January 28, 2009

Where is all that money going?

I have been hearing about the profligate spending that is the Reinvestment and Reconstruction proposal more popularly called the "economic stimulus plan". So, I decided to investigate what they are proposing.

Here's the marked up summary of the proposal from the House Appropriations Committee, and of the tax portion from the house Ways and Means Committee. Obviously, this will change by the time of its passing.

The bad news, for people earning over $75K ($150K for married couples filing jointly), there is very little relief. Let's see if Obama lives up to his campaign promise of lowering taxes for everyone with income under $250K. It all depends on how they phase the relief out.

Here are some highlights of what they are proposing (I have highlighted in blue, those provisions that individuals earning more than $75K per capita would benefit from):

Here's the marked up summary of the proposal from the House Appropriations Committee, and of the tax portion from the house Ways and Means Committee. Obviously, this will change by the time of its passing.

The bad news, for people earning over $75K ($150K for married couples filing jointly), there is very little relief. Let's see if Obama lives up to his campaign promise of lowering taxes for everyone with income under $250K. It all depends on how they phase the relief out.

Here are some highlights of what they are proposing (I have highlighted in blue, those provisions that individuals earning more than $75K per capita would benefit from):

Taxation (these dollar amounts represent the cost over 10 years):

- $145 BN on a tax credit of 6.2% of earned income phasing out for people earning over $75K ($150K for married couples filing jointly);

- $4.60 BN on increase in earned income tax credits for very poor families;

- $18 BN on increasing child credit;

- $13 BN for college education assistance;

- $2.56 BN for assistance to first time home buyers;

- $27 BN for small businesses and acquiring companies;

- $50 BN for local and state government assistance;

- $16 BN on renewable energy investments;

- $4.27 BN on upto 30% tax credit capped to $1500 per annum on energy efficient improvements to existing homes, e.g. heaters, air conditioners, etc.

- $54 BN on cleaner and more efficient energy (there is a small amount set aside to subsidize energy star appliances);

- $16 BN on science, technology and Internet access;

- $90 BN on improving roads, bridges and waterways;

- $141.6 BN on improving educational facilities and educational programs for poor and under privileged;

- $24.1 BN on improving healthcare services - particularly their computer systems;

- $102 BN in unemployment and hunger prevention benefits;

- $91 BN in preventing lay-offs in the public sector - state and local governments;

A few things to note:

First, the $800 BN number being thrown around is misleading. The cost of the tax proposals is over 10 years. The summary released by the Appropriation Committee on the spending proposals don't explicitly state how these costs will be phased. MSNBC suggested on Hardball that a substantial portion of it will not get spent till Obama's second term.

If we assume that the tax benefits would more or less be uniform over the 10 years or even skewed a little to later years, assuming economic growth and that 80% of the spending would be over the next one or three years, this would mean that the actual impact over the next two years of the stimulus is probably more like: $450 BN - $550 BN. Worse, over $100 BN is actually just preventing cut backs in government spending. So, it isn't incremental spend. The incremental spend is more like, $350 BN - $450 BN. Worse, this is spread over two to three years, which means that the immediate impact is likely $150 BN to $200 BN, which is just about 1.5% of GDP. Given the expected contraction in GDP is 1.6%, this seems low to spur growth. It'll just about cover the gap.

In terms of who gets the benefit, if you ignore timing differences, here's the allocation:

Tax cuts for individuals: 20%

Education: 19%

State and local governments: 18%

Underprivileged: 13%

Basic infrastructure: 11%

Renewable energy: 9%

Small businesses: 3%

Healthcare: 3%

Science and technology: 2%

Unfortunately, most individuals won't see most of these benefits for a while yet, whereas the spending increases will take near immediate effect.

Monday, January 26, 2009

On the economic recovery plan etc.

For those who are struggling with history of recession solutions ranging from Supply Side economics to Keynesian economics, this is an excellent brief map of the history of recession management in the US since the 1960s. Kennedy was actually the first President to consciously try a Keynesian solution to a recession. The other President to use it extensively was Reagan (in effect, although not in intent).

I don't know about you, but I am increasingly exasperated by the certitude with which talking heads on TV make assertions reiterating partisan rhetoric on the "economic rescue plan". Why do experts of all hues insist on peddling opinions as fact, despite the complete lack of evidence? Why not reproduce the facts in an intelligible way and leave it for viewers to decide? The truth is they don't know the answers, despite their protestations to the contrary.

Here's Warren Buffet on the topic of the economy. I've reproduced one part of the interview for you below:

I don't know about you, but I am increasingly exasperated by the certitude with which talking heads on TV make assertions reiterating partisan rhetoric on the "economic rescue plan". Why do experts of all hues insist on peddling opinions as fact, despite the complete lack of evidence? Why not reproduce the facts in an intelligible way and leave it for viewers to decide? The truth is they don't know the answers, despite their protestations to the contrary.

Here's Warren Buffet on the topic of the economy. I've reproduced one part of the interview for you below:

Q: "... But there is debate about whether there should be fiscal stimulus, whether tax cuts work or not. There is all of this academic debate among economists. What do you think? Is that the right way to go with stimulus and tax cuts?"

Warren Buffet: "The answer is nobody knows. The economists don’t know. All you know is you throw everything at it and whether it’s more effective if you’re fighting a fire to be concentrating the water flow on this part or that part. You’re going to use every weapon you have in fighting it. And people, they do not know exactly what the effects are. Economists like to talk about it, but in the end they’ve been very, very wrong and most of them in recent years on this. We don’t know the perfect answers on it. What we do know is to stand by and do nothing is a terrible mistake or to follow Hoover-like policies would be a mistake and we don’t know how effective in the short run we don’t know how effective this will be and how quickly things will right themselves. We do know over time the American machine works wonderfully and it will work wonderfully again."

Couldn't agree with him more.

On a different note, the complexity of the economic woes has been excellently summarized by Samuelson in his Op-ed piece. As Samuelson astutely points out, the US is facing three separate economic crises:

- A decline in consumer spending. Consumer spending is 70% of the US economy. With the wiping off of over $7 trillion in personal wealth, people just aren't spending any more.

- A breakdown of the financial system. Financial institutions just aren't lending, and without credit, there is little chance of growth. Part of this has to do with ravaged balance sheets due to mounting losses - the target of the TARP. Part of this has to do with the loss in confidence in several market making derivative and other financial instruments. And, a major part has to do with the uncertainties around people and companies' income potential and the consequential difficulty in developing appropriate lending criteria.

- Slowdown in the rest of the world: This is no longer just a US crisis. The rest of the world is slowing down. While a much smaller part of the US economy, the slowdown in the rest of the world could thwart attempts to kick start growth in the US.

Finally, let's clear up the confusion between the New Deal and Keynesian economics.

Although, Maynard Keynes did advise FDR he was neither the primary advisor to FDR nor the architect of the New Deal. Keynes inter alia advocated massive deficit spending and government intervention to ensure full employment as a means of reversing the depression. As this brief history of the New Deal in Wikipedia suggests, FDR didn't exactly do that. In fact, the US was very conservative in its approach and even tried to return to balanced budgets in the mid-1930s, with disastrous consequences. It is true that many of the structures that regulate today's economy were set up or restructured during the New Deal. However, as an example of Keynesian economics, the New Deal provides at best mixed data that can be sampled to buttress claims by both sides of the argument. The equivalence of the New Deal with Keynesian economics therefore is somewhat misguided.

Rush Limbaugh

These are the two interviews of Rush Limbaugh (The far right radio host currently in news because of his comments on Obama). The intereviews were with Sean Hannity on Fox news which I somehow managed to tune into. He clarifies his full stand on Obama's policies, questions the credentials, and expresses disappointment with Republicans taking an increasingly moderate stand to win 'acceptance'. Although taken with a grain of salt, I do see his point - not sure if I fully agree though! I thought it would be ineteresting for you guys to hear the 'other' point of view.

Part 1:

Part 2:

Part 1:

Part 2:

Friday, January 23, 2009

Gaza conflict - stock take

The conflict in Gaza usually evokes responses along long drawn battle lines. The Israelis and their supporters and sympathisers point to the horror of living under constant fear of death, and ask whether they don't have the right to defend themselves. The Palestinians point to the Israeli excesses and ask whether they don't have the right to defend themselves. Of course, like all true moral dilemmas, they both have a point.

However, the following statistics posted by the BBC puts this conflict into sharper relief:

- Thirteen Israelis killed

- More than 1,300 Palestinians killed

- More than 4,000 buildings destroyed in Gaza, more than 20,000 severely damaged

- 50,000 Gazans homeless, and

- 400,000 Gazans without running water

Until the Israeli offensive began, not one Israeli had been killed.

It seems that the Israelis could a 100:1 ratio of deaths justifiable in their retaliation. Most bizarrely, by Israel's own admission, they didn't take down any significant portion of Hamas' leadership. What in the world were the Israelis thinking before they started this carnage?

Tuesday, January 20, 2009

Inaugural address

Here is Obama taking the oath of office:

Here is Obama's inaugural address, for those who missed it:

This was in many ways one of the most anticipated speeches in history. While some, such as Mitch McConnel expressed some distaste about Obama's characterization of the current ills, it in most part lived upto the expectations of the occasion. Meanwhile, Sen. Edward Kennedy's collapse during the inaugural lunch was a sad note to an otherwise hopeful occasion.

Here's the text of the speech.

One interesting tidbit is that during the oath of office Obama appears to stumble over the oath. It turns out that the Chief Justice had changed the words of the oath.

The actual oath reads: "I, [name], do solemnly swear (or affirm) that I will faithfully execute the office of President of the United States, and will to the best of my ability, preserve, protect, and defend the Constitution of the United States."

Here's what the Chief Justice actually said: "... that I will execute the office of president to the United States faithfully".

Obama starts by saying, "... that I will execute ..." but then hesitates. The Chief Justice helpfully prompts with "faithfully execute the office of president of the United States ..." This latter version is correct.

Unfortunately, having already said, "... that I will execute ..." Obama could either repeat a corrected version of his earlier phrase or repeat a slightly modified version. He opted for the latter coming back with: "... the office of president of the United States faithfully ..."

On TV, it looks as if Obama is stumbling, but it looks as if Obama was stumped because the Chief Justice had got his words wrong.

On a different note, at one point in the inaugural address, Obama does err when he says, "Forty-four Americans have now taken the presidential oath." Oops. That's not exactly correct. One of the US Presidents, Grover Cleveland, won in 1885, lost in 1889 and won again in 1893. He served two terms, but not concurrently, and is counted as both the 22nd and the 24th President. So, although Obama is the 44th President, he is only the 43rd American to hold the office.

Here is Obama's inaugural address, for those who missed it:

This was in many ways one of the most anticipated speeches in history. While some, such as Mitch McConnel expressed some distaste about Obama's characterization of the current ills, it in most part lived upto the expectations of the occasion. Meanwhile, Sen. Edward Kennedy's collapse during the inaugural lunch was a sad note to an otherwise hopeful occasion.

Here's the text of the speech.

One interesting tidbit is that during the oath of office Obama appears to stumble over the oath. It turns out that the Chief Justice had changed the words of the oath.

The actual oath reads: "I, [name], do solemnly swear (or affirm) that I will faithfully execute the office of President of the United States, and will to the best of my ability, preserve, protect, and defend the Constitution of the United States."

Here's what the Chief Justice actually said: "... that I will execute the office of president to the United States faithfully".

Obama starts by saying, "... that I will execute ..." but then hesitates. The Chief Justice helpfully prompts with "faithfully execute the office of president of the United States ..." This latter version is correct.

Unfortunately, having already said, "... that I will execute ..." Obama could either repeat a corrected version of his earlier phrase or repeat a slightly modified version. He opted for the latter coming back with: "... the office of president of the United States faithfully ..."

On TV, it looks as if Obama is stumbling, but it looks as if Obama was stumped because the Chief Justice had got his words wrong.

On a different note, at one point in the inaugural address, Obama does err when he says, "Forty-four Americans have now taken the presidential oath." Oops. That's not exactly correct. One of the US Presidents, Grover Cleveland, won in 1885, lost in 1889 and won again in 1893. He served two terms, but not concurrently, and is counted as both the 22nd and the 24th President. So, although Obama is the 44th President, he is only the 43rd American to hold the office.

Friday, January 16, 2009

Woodward's management guide

In this piece in the Washingtonpost, Bob Woodward has outlined some lessons from the Bush years for Barack Obama. It makes a fascinating read.

We may quibble about whether Bush's failures are a nail in the coffin for conservatism, but there can be little doubt about the utter mismanagement of the Bush adminsitration. In his distillation of some key Bush failures, Woodward has identified some gems that are relevant not just for presidents, but all general managers. The list below is a distilled version paraphrased for managers instead of for the President:

We may quibble about whether Bush's failures are a nail in the coffin for conservatism, but there can be little doubt about the utter mismanagement of the Bush adminsitration. In his distillation of some key Bush failures, Woodward has identified some gems that are relevant not just for presidents, but all general managers. The list below is a distilled version paraphrased for managers instead of for the President:

- Managers set the tone. Don't be passive or tolerate virulent divisions among subordinates and team members.

- Insist that subordinates speak out loud in front of the others, even - or especially - when there are vehement disagreements.

- Master the fundamental ideas and concepts behind policies. Don't farm out the understanding of the ramifications and trade-offs.

- Draw people out to ensure that bad news surfaces in a timely manner.

- Foster a culture of skepticism and doubt. Doubt is not the enemy of good policy; it can help leaders evaluate alternatives, handle big decisions and later make course corrections if necessary.

- Be rigorous about reconciling differences in contradictory data.

- Be willing to tell the hard truth to stakeholders, even if that means delivering very bad news.

- Righteous motives are not enough for effective policy.

- Insist on strategic thinking - i.e. define where the organization should be in one, two or four years (depending on the level) and develop a detailed tactical plans to get there. It's easy to become consumed with putting out brush fires, but in the long run managers will be judged by the success of their long-range plans, not their daily crisis management.

- Embrace transparency.

A breakdown in classical economics

Very nice article by David Brooks, neatly summarizing the breakdown in classical economics and why the answers to the current crisis may lie more in behavioral economics.

Wednesday, January 14, 2009

Bushisms

Reading this article in Slate made me realize how much I will miss President Bush's wonderful turn of phrase. Rarely has there been a leader, let alone a leader of the free world, who committed so many oratory gaffes. Surprisingly though, while these were quite clearly unintended, some of them seem strangely prescient and insightful in the light of what followed or what was being referenced.

First use of telescope

For years, Galileo has been credited as being the first man to observe the moon through a telescope and to make detailed drawings of the moon. Now it seems that Thomas Harriot, a wealthy Englishman, had made very detailed drawings of the moon's surface well before Galileo.

The discussion in the article ponders why Galileo is so famous and not Thomas Harriot. Unfortunately, this is often true in Science. Darwin, though he did write the most comprehensive work on the origin of species, was not the first to come up with the ideas. There are several preceding claims. Similarly, Marconi probably wasn't the first to invent the telegraph. Newton and Leibnitz both arrived at entirely different formulations for calculus (and a lot of what we use today is based on Leibnitz and not Newton). One could go on and on.

It is curious, but it does seem that often scientific breakthroughs have been arrived at somewhat independently by multiple people at the same time. The person usually credited is usually not the person who was first, but the person who did the most to popularize the breakthrough. In that sense, it is right that Galileo is the one credited.

The discussion in the article ponders why Galileo is so famous and not Thomas Harriot. Unfortunately, this is often true in Science. Darwin, though he did write the most comprehensive work on the origin of species, was not the first to come up with the ideas. There are several preceding claims. Similarly, Marconi probably wasn't the first to invent the telegraph. Newton and Leibnitz both arrived at entirely different formulations for calculus (and a lot of what we use today is based on Leibnitz and not Newton). One could go on and on.

It is curious, but it does seem that often scientific breakthroughs have been arrived at somewhat independently by multiple people at the same time. The person usually credited is usually not the person who was first, but the person who did the most to popularize the breakthrough. In that sense, it is right that Galileo is the one credited.

Stonehenge in the US?

It seems that there are rumors of a weird underwater circular stone structure discovered in Lake Michigan. Some are hypothesizing that this is a US version of Stonehenge. It's probably a hoax though, although were it to be true, it would make a very interesting discovery.

Wednesday, January 7, 2009

Satyam Shivam ... oh nevermind!

The irony in a name. Per Satyam's chairman ... they've been massively inflating earnings for years.

Read more about it here.

Read more about it here.

Tuesday, January 6, 2009

History according to the vanquished

The common view of science in the West is that the world discovered science only with the advent of Newton, Descartes, Copernicus, Kepler, etc. The truth, however, is somewhat more murky. This article by Jim Al-Khalili discusses the contributions of al-Hassan Ibn al-Haytham, an Iraqi scholar who lived in the 10th century AD, who had experimentally proven many of the findings about light and celestial bodies that Newton later describes in his works. He even invents a pin-hole camera. What the article fails to discuss is whether these ideas influenced Newton. They may well have, even if it was in oblique ways. Newton was an avid reader and his reading included ideas by many foreign authors. Ideas are memes. They percolate and survive, often skipping cultural barriers in unexpected ways.

Monday, December 29, 2008

More motgage trouble

In this article, the author discusses the Alt-A mortgage resets, which are expected to peak in 2009-2010. Essentially the author argues another risk uptick is in the offing which will throw a bunch of currently healthy people in a mess, particularly in a worsening economy. Not sure how credible the data is.

If this is true, can this averted? Well, maybe. One difference between the Alt-A resets and the subprime mortgage resets is the ability of the borrowers to refinance. If the US government is able to get Fannie Mae and Freddie Mac to lower refinance rates and create sufficient liquidity, some of the impact of the reset may be offset. If, if, if ...

If this is true, can this averted? Well, maybe. One difference between the Alt-A resets and the subprime mortgage resets is the ability of the borrowers to refinance. If the US government is able to get Fannie Mae and Freddie Mac to lower refinance rates and create sufficient liquidity, some of the impact of the reset may be offset. If, if, if ...

Sunday, December 28, 2008

Ironical kill by great white

Will ironies never cease. First, the famous environmentalist and naturalist Steve 'crocodile hunter' Irvin was killed by a ray in 2006. Now Brian Guest, a naturalist who campaigned to rescue Great White sharks, was eaten by one while swimming only meters away from his son off the coast of Australia. The article gives a gruesome account of his death.

He reportedly wrote on the Western Angler website forum in 2004: "I have always had an understanding with my wife that if a shark or ocean accident caused my death then so be it, at least it was doing what I wanted. Every surfer, fisherman and diver has far more chance of being killed by bees, drunk drivers, teenage car thieves and lightning. Every death is a tragedy – regardless of the cause – but we have no greater claim to use of this earth than any of the other creatures [we] share it with."

It doesn't seem as if the Great Whites discern between their friends and enemies in picking their meals.

He reportedly wrote on the Western Angler website forum in 2004: "I have always had an understanding with my wife that if a shark or ocean accident caused my death then so be it, at least it was doing what I wanted. Every surfer, fisherman and diver has far more chance of being killed by bees, drunk drivers, teenage car thieves and lightning. Every death is a tragedy – regardless of the cause – but we have no greater claim to use of this earth than any of the other creatures [we] share it with."

It doesn't seem as if the Great Whites discern between their friends and enemies in picking their meals.

Saturday, December 27, 2008

Fear of cliffs

If you expected an article about the white cliffs of Dover, you will be sorely disappointed. I am referring here to cliff events in the context of the economy.

In recent days there have been frantic efforts by many in the government egged on by many reputed economists including advocates of free markets to intervene in the market and prop up failing institutions. They have intervened, but seemingly to little effect. What's going on? Why is there such a panic?

Underlying the theory of free markets is an assumption that free markets, even when not perfectly efficient, are mean reverting. This is why advocates of non-intervention speak of "market correction". The idea is that while there can be a distortion in value for a time, ultimately everything will automatically revert to a true value. Of course, this view assumes the existence of such am invariant 'true value'.

There is, however, a more interesting set of theories that have been evolving that postulate that natural systems, including financial markets are chaotic. This means, that while they may occasionally appear to be mean reverting, there is no reason that they should revert to a mean. Instead, even small changes can have extremely magnified effects resulting in a different level in the long run. In such systems, small changes can have huge, often catastrophic effects. Examples of such chaotic changes are literally the straw that breaks the camel's back or the butterfly effect. In this view, there are times when a financial system like the economy can stand at a brink, where on one side, it seems unwell but curable, and on the other it faces complete ruin.

Let me illustrate with an example.

In the early part of this decade, as Enron devolved into a financial debacle, disclosures made to ratings agencies put the ratings agencies in a quandary. On the one hand, if they continued to maintain the same credit rating, then it was possible that in the interim time the company could find a way to pull itself out of the mess. On the other hand, if they reduced the rating, then it would automatically trigger a series of obligations that would hinder Enron's ability to borrow. The resulting mess would lead to further downgrades, and so on, quickly reducing Enron to junk bond status.

This was an example of a credit cliff. It's a situation where a small change in the conditions, i.e. Enron's credit rating, could push it over a cliff.

Two things to note.

The problem is that the US economy as a whole is over-leveraged and over valued. The US need a HUGE amount of money to dig itself out. The only way for the US to get that money is that everyone continues to believe in the US.

With huge foreign holdings of US debt and US investments, if people suddenly started to doubt the US and started to disinvest, then the US economy could, in theory, collapse. The problem is that unlike the mean reverting view, in this view, the new equilibrium would leave the faith in the US economy so damaged that it would permanently destroy the US economy's value, and the US would never completely recover.

The Fed's experiment with Lehman caused a crash that has everyone spooked. They won't try it again. No other large US brand name can be allowed to fail. What the US government, Fed and all those illustrious economists are hoping is that if they can just hold on long enough, things will get better. They are banking on the assumption that it's in no one's interest to let the US fail. The alternative is a complete collapse of the US economy.

Are we really at such a cliff? Who knows? But you don't really want to find out by stepping off the ledge, do you?

However, note that all these interventions maintain a fiction. They keep you on the right side of the ledge. They don;t get you further away from the ledge. In fact, in some ways, they lift you up a bit, making the fall, if it comes, all the worse. So long as there is no catastrophic collapse of the economy, you could say these measures are working. But you are still at the edge.

To fix things, we still need to fix the underlying problem - asset price inflation. There are only two solutions. Either let the asset prices deflate. Or, let them stagnate until the value increases to the price. Neither is attractive. Both take time, maybe years. And, remember the second lesson from Enron is that ultimately the fiction can only maintained for so long. Let's hope the creditors of the US economy are more patient.

In recent days there have been frantic efforts by many in the government egged on by many reputed economists including advocates of free markets to intervene in the market and prop up failing institutions. They have intervened, but seemingly to little effect. What's going on? Why is there such a panic?

Underlying the theory of free markets is an assumption that free markets, even when not perfectly efficient, are mean reverting. This is why advocates of non-intervention speak of "market correction". The idea is that while there can be a distortion in value for a time, ultimately everything will automatically revert to a true value. Of course, this view assumes the existence of such am invariant 'true value'.

There is, however, a more interesting set of theories that have been evolving that postulate that natural systems, including financial markets are chaotic. This means, that while they may occasionally appear to be mean reverting, there is no reason that they should revert to a mean. Instead, even small changes can have extremely magnified effects resulting in a different level in the long run. In such systems, small changes can have huge, often catastrophic effects. Examples of such chaotic changes are literally the straw that breaks the camel's back or the butterfly effect. In this view, there are times when a financial system like the economy can stand at a brink, where on one side, it seems unwell but curable, and on the other it faces complete ruin.

Let me illustrate with an example.

In the early part of this decade, as Enron devolved into a financial debacle, disclosures made to ratings agencies put the ratings agencies in a quandary. On the one hand, if they continued to maintain the same credit rating, then it was possible that in the interim time the company could find a way to pull itself out of the mess. On the other hand, if they reduced the rating, then it would automatically trigger a series of obligations that would hinder Enron's ability to borrow. The resulting mess would lead to further downgrades, and so on, quickly reducing Enron to junk bond status.

This was an example of a credit cliff. It's a situation where a small change in the conditions, i.e. Enron's credit rating, could push it over a cliff.

Two things to note.

- Firstly, the cliff was characterized by the value was driven belief that was ultimately self referential - i.e. it had value because people believed it had value. It was solvent as long as people believed that it was and would continue to be solvent.

- Secondly, the fiction was ultimately unsustainable.

The problem is that the US economy as a whole is over-leveraged and over valued. The US need a HUGE amount of money to dig itself out. The only way for the US to get that money is that everyone continues to believe in the US.

With huge foreign holdings of US debt and US investments, if people suddenly started to doubt the US and started to disinvest, then the US economy could, in theory, collapse. The problem is that unlike the mean reverting view, in this view, the new equilibrium would leave the faith in the US economy so damaged that it would permanently destroy the US economy's value, and the US would never completely recover.

The Fed's experiment with Lehman caused a crash that has everyone spooked. They won't try it again. No other large US brand name can be allowed to fail. What the US government, Fed and all those illustrious economists are hoping is that if they can just hold on long enough, things will get better. They are banking on the assumption that it's in no one's interest to let the US fail. The alternative is a complete collapse of the US economy.

Are we really at such a cliff? Who knows? But you don't really want to find out by stepping off the ledge, do you?

However, note that all these interventions maintain a fiction. They keep you on the right side of the ledge. They don;t get you further away from the ledge. In fact, in some ways, they lift you up a bit, making the fall, if it comes, all the worse. So long as there is no catastrophic collapse of the economy, you could say these measures are working. But you are still at the edge.

To fix things, we still need to fix the underlying problem - asset price inflation. There are only two solutions. Either let the asset prices deflate. Or, let them stagnate until the value increases to the price. Neither is attractive. Both take time, maybe years. And, remember the second lesson from Enron is that ultimately the fiction can only maintained for so long. Let's hope the creditors of the US economy are more patient.

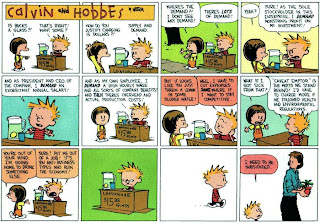

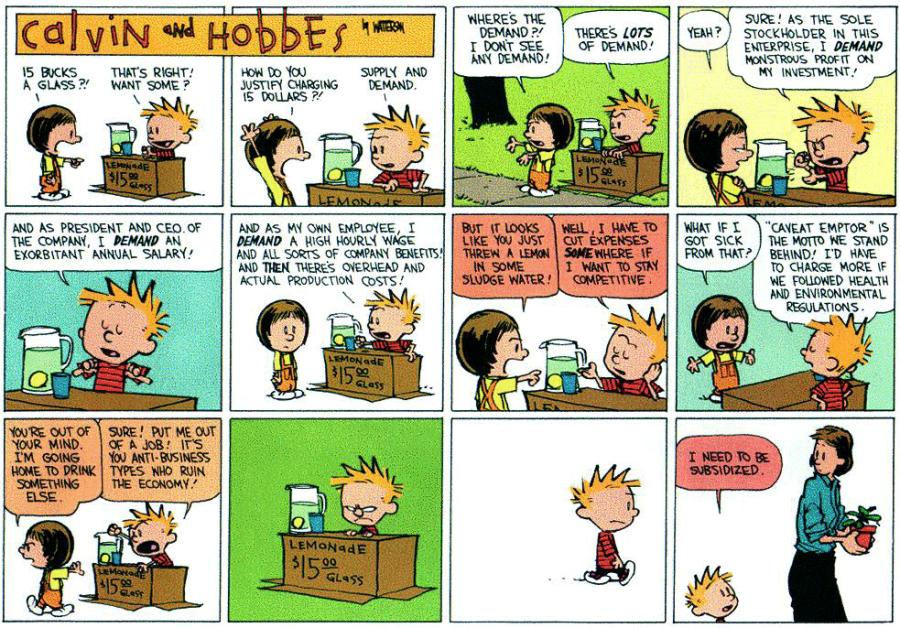

On the bailouts ...

Dhakks and I were having a discussion recently on the bailouts, and I was almost inspired to write a lengthy piece explaining my views. But then I came across this Calvin and Hobbes strip that does it so much better. Enjoy! (click on the strip to expand)

{kind=link}

Wednesday, December 17, 2008

Should India receive a Dinosaur Tax?

I've often heard the idea toyed around that the world should perhaps pay Brazil an oxygen tax. No, the UN isn't seriously contemplating that.

But now, methinks, the world owes India a Dinosaur Tax. There's new evidence that suggests lava flows, and related sulfur emissions, in India led to the decline of dinosaurs.

It's a nascent investigation but you can read more about it here.

But now, methinks, the world owes India a Dinosaur Tax. There's new evidence that suggests lava flows, and related sulfur emissions, in India led to the decline of dinosaurs.

It's a nascent investigation but you can read more about it here.

Tuesday, December 16, 2008

Fun stuff

With the economy tanking, consumer prices falling by the largest amount in 50 years, the Fed cutting rates to unheard of levels (apparently unaware of the complete failure of supply side economics over the last year), and Madoff adding to gloom and doom, I thought something more entertaining may be in order.

Dick Cavett recently got an earful for his amusing piece, "The Wild Wordsmith of Wasilla" where he explores gems such as: "My concern has been the atrocities there in Darfur and the relevance to me with that issue as we spoke about Africa and some of the countries there that were kind of the people succumbing to the dictators and the corruption of some collapsed governments on the continent, the relevance was Alaska’s investment in Darfur with some of our permanent fund dollars." It's stuff you can't make up.

His latest piece on Gov. Blagojevich is equally amusing, as he ponders, "The question overhanging this sordid mess, you might agree, is, “How did such a specimen ever get elected?”

It’s as if a soldier, tested for his fitness as potential combat leader, passed his physical despite scurvy, pyorrhea, Jake leg, leprosy, the quinsy, contagious influenza and at least two trick knees."

It's just what I was wondering.

And, if you missed it, President Bush provided his contribution with the famous shoe ducking incident, which just about summarises his presidency.

Dick Cavett recently got an earful for his amusing piece, "The Wild Wordsmith of Wasilla" where he explores gems such as: "My concern has been the atrocities there in Darfur and the relevance to me with that issue as we spoke about Africa and some of the countries there that were kind of the people succumbing to the dictators and the corruption of some collapsed governments on the continent, the relevance was Alaska’s investment in Darfur with some of our permanent fund dollars." It's stuff you can't make up.

His latest piece on Gov. Blagojevich is equally amusing, as he ponders, "The question overhanging this sordid mess, you might agree, is, “How did such a specimen ever get elected?”

It’s as if a soldier, tested for his fitness as potential combat leader, passed his physical despite scurvy, pyorrhea, Jake leg, leprosy, the quinsy, contagious influenza and at least two trick knees."

It's just what I was wondering.

And, if you missed it, President Bush provided his contribution with the famous shoe ducking incident, which just about summarises his presidency.

Monday, December 15, 2008

The $50BN fraud

This is the latest scandal to hit Wall Street. The facts are simple. Bernard Madoff, a hedge fund manager, has for years apparently run one of the biggest scams on wall street. He essentially took money from new investors and paid off older investors with it. The entire house of cards has collapsed with the fall in the world markets. The aggregate losses to investors, which includes some big names across the world, is estimated to be $50BN. He has been arrested, and is out on bail.

The puzzling part is that for years, investors, bankers, lawyers, IRS agents and auditors all scrutinized his books and concluded he was completely above board. The fact that this could continue for years (some estimate 10+ years) without alerting any regulators has investors shaken. The BBC is reporting that this has shaken foreign investors' confidence in the US regulatory system to an extent that could potentially have serious consequences for the US.

By the way, this is a classic Ponzi scheme. A Ponzi scheme is one where you delude people into thinking you are making them money by paying them off with money from incoming investors. You can keep this going so long as everyone trusts you.

The term "Ponzi scheme" refers to Charles Ponzi. Charles Ponzi was by no means the first to conceive of this. However, he did do it more extravagantly than most. In 1920, he was involved in a scheme to make money off arbitrage on postage stamps that promised to "double your money in 90 days". He realized soon enough though that he didn't actually need to buy the postage stamps and exchange them as he promised. He could do it on his books and everyone would go along with him. So, he kept paying off people with the money he collected from incoming investors. Ultimately, his scheme collapsed leading to his ruin, arrest and jail. He died in poverty in Brazil. Before he died, he is reputed to have told a reporter, "Even if they never got anything for it, it was cheap at that price. Without malice aforethought I had given them the best show that was ever staged in their territory since the landing of the Pilgrims! It was easily worth fifteen million bucks to watch me put the thing over."

The puzzling part is that for years, investors, bankers, lawyers, IRS agents and auditors all scrutinized his books and concluded he was completely above board. The fact that this could continue for years (some estimate 10+ years) without alerting any regulators has investors shaken. The BBC is reporting that this has shaken foreign investors' confidence in the US regulatory system to an extent that could potentially have serious consequences for the US.

By the way, this is a classic Ponzi scheme. A Ponzi scheme is one where you delude people into thinking you are making them money by paying them off with money from incoming investors. You can keep this going so long as everyone trusts you.

The term "Ponzi scheme" refers to Charles Ponzi. Charles Ponzi was by no means the first to conceive of this. However, he did do it more extravagantly than most. In 1920, he was involved in a scheme to make money off arbitrage on postage stamps that promised to "double your money in 90 days". He realized soon enough though that he didn't actually need to buy the postage stamps and exchange them as he promised. He could do it on his books and everyone would go along with him. So, he kept paying off people with the money he collected from incoming investors. Ultimately, his scheme collapsed leading to his ruin, arrest and jail. He died in poverty in Brazil. Before he died, he is reputed to have told a reporter, "Even if they never got anything for it, it was cheap at that price. Without malice aforethought I had given them the best show that was ever staged in their territory since the landing of the Pilgrims! It was easily worth fifteen million bucks to watch me put the thing over."

Subscribe to:

Comments (Atom)