In recent days, people on the left and the right have been coming out of the woodwork with advice galore for the administration. Obama has found friends in strange places. First, we have David Brooks expressing hope in Obama's Afghanistan strategy and declaring it a winnable war. This view gets support from Rachel Maddow at the other end of the spectrum. In her recent TV spot, she talked it up so much, it seemed like she was trying to sell it to herself.

Then we have Krugman declaring emphatically that Summers and the Obama team aren't taking the true lesson of the current mess - i.e. a fundamental repudiation of the market mystique.

Meanwhile, we have Michael Gerson defending Obama's use of the teleprompter, pointing out that a leader's attempt to express himself with precision is not a sign of a lack of genuineness, and neither is a politician's attempt to wing it anything but shallowness.

Michael Gerson's article I wholeheartedly agree with. The idea that a leader who thinks through what he or she is about to see is somehow less of a leader for relying on a script is laughable. It would be different if the assumption was that Obama wasn't intellectually able, but even his critics have to acknowledge his intellectual prowess.

On the war, I am less sanguine than these more upbeat assessments. Afghanistan is definitely where the US should focus, but remember that this is the region that handed the British and the Soviets their defeats. A protracted engagement in Afghanistan could be worse than both Iraq and Vietnam. Furthermore, wars are and always been massively draining on the national coffers. So, I would be more cautious in singing Obama's praise. The question in my mind is whether he can stay focused on achievable goals, or whether he will get distracted by idealistic fervour. As long as he is pragmatic, it should be fine.

Finally, on Krugman and the economy. I know that Krugman is not happy about the market mystique dominating. True market's need regulation. However, you have to only look at highly regulated markets around the world to realise that enabling the heavy hand of government is a cure that may be worse than the disease it attempts to cure. So, am I unhappy about Obama's hesitance? No. In fact, I am more concerned that he may be tempted to allow many of the more radical ideas proposed by Congress to pass. The question is whether he will be able to stand up to a Congress dominated by his own party, while still building consensus for his agenda. My guess - doubtful!

Showing posts with label Economy. Show all posts

Showing posts with label Economy. Show all posts

Saturday, March 28, 2009

Monday, March 23, 2009

Spitzer on the financial mess ...

OK ... so Elliot Spitzer proved to have questionable sexual morals and marital fidelity. But, in this interview, he makes some fascinating points. The basic point he is making is that there is no legislation that can compensate for regulatory incompetence or lack of will. If the executive does not enforce the laws, then the laws are moot. Ironic, but very true.

TARP version ... how many has it been again?

Timothy Geithner just announced his new TARP plan: $75BN to $100BN to back $500BN of funds to buy troubled assets. How is this different from the Paulson plan? It is a little more specific. It does leverage private capital. However, in essence, it is the same plan.

Here's how it would work:

Here's how it would work:

- Let's say a Bank seeks to sell pool of mortgages worth $100;

- A private auction decides that asset is now worth $84;

- The private investor and government put up $6 each;

- They then borrow remaining $72 from government;

- That loan is guaranteed against any losses;

- If asset is later sold at higher price, government makes profit and private investor pays back loan and pockets profit;

- If asset is sold at lower price, government and private investors could lose initial investment.

Am I missing something, or is this really saying:

- The government and the private investor share equally in all the gains on the entire $100;

- The government and the private investor share equally in losses till 14% of the market value at the auction, and

- The government foots the bill for any loss in excess of 14% of the value.

If this is right, it seems like a pretty good deal for investors if the market valuations now are relatively fair.

Krugman, meanwhile, is railing against the plan. I didn't quite follow his logic. His main argument seems to be that the banks will still have lost the money they have, and no amount of taking stuff off the books will help. True. But wouldn't the lack of exposure to further downside risk reduce the inter bank solvency issue somewhat? If Krugman has a reason to believe it won't, he didn't explain it in the article.

Krugman has pointed out that history has shown that some amount of nationalization is necessary.

Couple of points.

- Firstly, Krugman is right. Some form of nationalization is probably the most effective answer. Government guarantees / nationalization gives people confidence about the solvency of their counterparties. Geithner's plan does that too. However, the degree of confidence inspired by the former is far more and so, I would argue, it is a much quicker fix. Obama, however, needs to weigh the political expediency of nationalization and what it might do to his ability to get other policies passed. So, the fact that we haven't gone there may be just as much a political calculation as an economic one.

- Secondly, at one point in the article, Krugman writes: "And now Mr. Obama has apparently settled on a financial plan that, in essence, assumes that banks are fundamentally sound and that bankers know what they’re doing." [emphasis added] In so saying, Krugman betrays his political biases and, dare I say it, his naivete. Firstly, how can pouring $500 BN to $1 trillion into the banks in addition to billions already spent suggest that anyone in government think there is anything, fundamentally or otherwise, sound with the banks? But, maybe Krugman is reflecting on the competence of bankers, particularly senior management. In this context, I too have concerns, but is Krugman's idea any better? If we nationalize, who can we replace everyone in these organizations with? Would the bank actually operate better? Yes, they made bad bets, as did everyone else. Does that mean the government will do better? The same government who regulated these industries so 'brilliantly'?

I too am concerned that those who caused the mess are not paying a high enough cost. Having said that, there seems to be a tendency on the left to assume that just because one option is bad, the others are necessarily better. That's a logical fallacy. Krugman and others need to explain why they believe so. Also, nationalization may indeed solve the immediate crisis faster. However, would it really be the long term interest of the nation? Are nationalized banks really better banks?

My guess is that before this is over, a number of these banks and financial institutions are going to be nationalized. AIG and Citi effectively are already. Political expediency aside, more probably would have been already. However, I am not as convinced as Krugman that Obama's reticence to nationalize is necessarily a bad thing.

Monday, March 16, 2009

Ben speaks ...

It's almost unheard of for a sitting Fed Chairman to give an interview of any kind. This 60 Minutes interview with Ben Bernanke is an exception. Nothing startling, but still very interesting.

Wednesday, March 11, 2009

Law abiding citizen?

To some, what Cramer says may be shocking, to others, it may remind us why we think the blind belief in the rationality of markets is foolhardy. Can't say I was surprised. Here are some gems from an interview with Cramer.

Tuesday, March 10, 2009

Fun stuff in depressing times

Last week, Jon Stewart decided to rip into CNBC. By the end, I was left with more faith in astrology than the talking heads. It's one of his best segments this year ... hilarious!

Then, Cramer complained. He felt he was taken out of context. Huh? Baiting The Daily Show? Well, here's Jon Stewart's response. Poor Cramer. Why is he allowed on TV again?

On the subject of faith in things that are completely unsubstantiated, like "experts" on TV, here's Joel Stein critiquing the lack of faith in science of liberals. It is hugely entertaining and so very accurate.

Finally, I have been depressed of late of the complete dearth of conservative ideas that address the current economic woes. I was so relieved, therefore, to read David Brooks, finally, critique Obama's policies in an intelligent way. If only conservatives could have adopted such a posture, we might have the response we needed to the crisis instead of the response we settled on, which will probably prove inadequate (I hope I am proved wrong in this).

PS: I must give a shout out to Grain of Sand, who had presciently predicted in November that we would see the type of shocking performance of GM we have witnessed in recent weeks. It might have been cheaper to put the GM staff in the US on a government payroll and start from scratch! Chapter 11 anyone? It's what its there for.

Then, Cramer complained. He felt he was taken out of context. Huh? Baiting The Daily Show? Well, here's Jon Stewart's response. Poor Cramer. Why is he allowed on TV again?

On the subject of faith in things that are completely unsubstantiated, like "experts" on TV, here's Joel Stein critiquing the lack of faith in science of liberals. It is hugely entertaining and so very accurate.

Finally, I have been depressed of late of the complete dearth of conservative ideas that address the current economic woes. I was so relieved, therefore, to read David Brooks, finally, critique Obama's policies in an intelligent way. If only conservatives could have adopted such a posture, we might have the response we needed to the crisis instead of the response we settled on, which will probably prove inadequate (I hope I am proved wrong in this).

PS: I must give a shout out to Grain of Sand, who had presciently predicted in November that we would see the type of shocking performance of GM we have witnessed in recent weeks. It might have been cheaper to put the GM staff in the US on a government payroll and start from scratch! Chapter 11 anyone? It's what its there for.

Saturday, February 21, 2009

Worse than the Great Depression?

How bad are things? Well, in some ways its not quite as bad as the Great Depression. Unemployment now is officially around 7%, although including hidden unemployment its probably more like 14%. In the Great Depression, unemployment had touched 25%.

However, in other ways, economists are beginning to point out that it's much worse. Why? Well, for one things are moving faster than anyone imagined possible. Volcker points out that the global fall in industrial production is unprecedented and breaks even the worst doomsday predictions. George Soros points out that there is no end in sight to the financial crisis. The market capitalization of the banking sector now hovers at about what the government has pumped in.

The trouble is that admit that they don't really know what will work. At this point, everyone is trying their best and hoping a lot.

However, in other ways, economists are beginning to point out that it's much worse. Why? Well, for one things are moving faster than anyone imagined possible. Volcker points out that the global fall in industrial production is unprecedented and breaks even the worst doomsday predictions. George Soros points out that there is no end in sight to the financial crisis. The market capitalization of the banking sector now hovers at about what the government has pumped in.

The trouble is that admit that they don't really know what will work. At this point, everyone is trying their best and hoping a lot.

Friday, February 20, 2009

The stimulus package is too small

OK, I've said it before, and I'll say it again - the stimulus package passed by Congress is too small. President Obama should consider a second stimulus, and consider it fast. Don't believe me, here is the assessment buried in the minutes of Federal Reserve's most recent meeting of its open market committee:

Even otherwise, this makes it seem as if what the administration is shooting for is not recovery but stabilization. Not very inspiring!

Paul Krugman, who admittedly is not a fan of the scaled down plan, points out that with the package in place, the closest parallel is the Panic of 1873 which was a 5 year recession. That would mean we could be in a slump till 2012.“All participants anticipated that unemployment would remain substantially above its longer-run sustainable rate at the end of 2011, even absent further economic shocks; a few indicated that more than five to six years would be needed for the economy to converge to a longer-run path characterized by sustainable rates of output growth and unemployment and by an appropriate rate of inflation.” [emphasis added]

Even otherwise, this makes it seem as if what the administration is shooting for is not recovery but stabilization. Not very inspiring!

Wednesday, February 18, 2009

Mortgage relief plan

Friday, February 13, 2009

Difference in perspective

As I listened to the debate on the stimulus and the different sides of the story, it struck me as surprisingly reminiscent, in an interesting way, to the debate before the Iraq war. Let me explain.

During the run up to the Iraq war many had felt the war was justified and others had felt it was not. If one looks dispassionately at their debate, it becomes clear that their difference arose not so much because of differences in information or facts, but in differences in their perspective and assumptions about the nature of the underlying problem of terrorism, which consequently affected their subsequent evaluation of all data.

Those for the war genuinely believed that 9/11 was a game changing event. That an evil group of highly organized people had declared war on them, a group they called "terrorists" and consequently it justified a counter "war on terrorism." Moreover, this war was different and the old rules no longer applied. Driven by a fear of imminent attack, the people who subscribe to this view advocated and still advocate no rules, no surrender, and a relentless fight against the enemy. Consequently, the suspension of compliance with rules of engagement and treaties such as the Geneva convention, rules that had been inviolable against foes as formidable as the USSR, seem to be justified. Is the cost of a few civil liberties really worth a collossal loss of life?

On the other side were people who believed that 9/11 represent the act of a bunch of criminals who had taken advantage of some laxities in the system to conduct a spectacular but ultimately futile attack. These people look at 9/11 as the same as the attacks in UK, Spain, India, Indonesia, Egypt, Yemen, etc. To these people, terrorism is a law and order problem, not a military problem. The fight is against a relatively sparse minority of disenchanted and highly dangerous mercenaries, not governments. They saw and still see no threat to the American way of life, no need for rethinking the structures of government or treaties. The solution they advocate is coordinated police action, removing safe havens, and beefing security. Ultimately though, these people see terrorists as being in the same category as drug czars and not USSR.

Note, those in favor of the war believed the rules had changed and it was war, those on the other side believed nothing substantive had changed and that it was a law and order problem. This difference in perspective has defined the debate ever since.

Now, the bad news is that there are historical precedents to back both sides.

Backing the "everything is normal" camp is a bunch of historical data that essentially suggests that whether you do Keynisian intervention or monetary intervention, ultimately the market will find its own order, and that most recesssions are technical corrections that would probably revert to mean no matter what steps you take.

On the "the sky is falling" side, there are dramatic historical precedents of economies like Japan, where things were eerily similar to the conditions in the US today, and whose ravages are still being felt 15+ years after the fact. Add to that the fact that we have unprecedented monetary intervention, with interest rates no longer working and the Fed resorting to quantitative easing. We have massive fiscal deficits as far as the eye can see adding to the already burgeoning national debt. All of which calls into question how much wiggle room the government will have after the current suite of programs.

At the end of the day though, no one can truly claim to "know" with any degree of certainty which view is correct.

However, we can consider the pay-offs of different courses of action.

The more interesting thing is that Obama has opted for a middle road. As Paul Krugman (who is firmly in the "sky is falling" camp) explains, the current stimulus doesn't do much to plug the $2.9 trillion gap in the GDP projected by the CBO. For the roughly $600BN that will actually injected into the economy as part of the current stimulus package to actually be effective in plugging this gap, you need to assume that the velocity of money will be retained at current levels, i.e. it assumes that savings rates won't rise by too much. If you look at depressions, then that seems like a ridiculously optimistic presumption.

So, Obama is hedging his bets. This seems like a lose-lose proposition to me. If the "sky is falling" camp is right, then this won't be enough. If the "everything is normal" camp is right, it'll be too much. Net net, this will neither guarantee a rescue nor guarantee that we avoid the ills of overspending. Now, Obama may believe that the truth lies in the center and that a cautious incremental approach is better. And he may well be right. But he is banking on being able to get more legislation through Congress if and when the need arises. Let's hope he is right!

During the run up to the Iraq war many had felt the war was justified and others had felt it was not. If one looks dispassionately at their debate, it becomes clear that their difference arose not so much because of differences in information or facts, but in differences in their perspective and assumptions about the nature of the underlying problem of terrorism, which consequently affected their subsequent evaluation of all data.

Those for the war genuinely believed that 9/11 was a game changing event. That an evil group of highly organized people had declared war on them, a group they called "terrorists" and consequently it justified a counter "war on terrorism." Moreover, this war was different and the old rules no longer applied. Driven by a fear of imminent attack, the people who subscribe to this view advocated and still advocate no rules, no surrender, and a relentless fight against the enemy. Consequently, the suspension of compliance with rules of engagement and treaties such as the Geneva convention, rules that had been inviolable against foes as formidable as the USSR, seem to be justified. Is the cost of a few civil liberties really worth a collossal loss of life?

On the other side were people who believed that 9/11 represent the act of a bunch of criminals who had taken advantage of some laxities in the system to conduct a spectacular but ultimately futile attack. These people look at 9/11 as the same as the attacks in UK, Spain, India, Indonesia, Egypt, Yemen, etc. To these people, terrorism is a law and order problem, not a military problem. The fight is against a relatively sparse minority of disenchanted and highly dangerous mercenaries, not governments. They saw and still see no threat to the American way of life, no need for rethinking the structures of government or treaties. The solution they advocate is coordinated police action, removing safe havens, and beefing security. Ultimately though, these people see terrorists as being in the same category as drug czars and not USSR.

Note, those in favor of the war believed the rules had changed and it was war, those on the other side believed nothing substantive had changed and that it was a law and order problem. This difference in perspective has defined the debate ever since.

I remember listening to a commentator on TV who talked about the merits of competition of ideas, about how this really is the strength of democracy. The assumption was that there was an objective way of evaluating the data and rationally resolving the dispute. Yet, when one has such different perspectives, it isn't a data problem, it is a measurement or scale problem. The two sides value the benfits and costs in fundamentally different ways. So, it is nearly impossible to reconcile the problem with data alone.

There is a similar dissonance today in the economic debate. One group genuinely believes that this recession is like most others, just a bit deeper. That nothing really has changed. On the other side is a group that believes that there are fundamental structural issues that make this recession unlike any other since the Great Depression. What your view of the problem is colors the view of the solution.Now, the bad news is that there are historical precedents to back both sides.

Backing the "everything is normal" camp is a bunch of historical data that essentially suggests that whether you do Keynisian intervention or monetary intervention, ultimately the market will find its own order, and that most recesssions are technical corrections that would probably revert to mean no matter what steps you take.

On the "the sky is falling" side, there are dramatic historical precedents of economies like Japan, where things were eerily similar to the conditions in the US today, and whose ravages are still being felt 15+ years after the fact. Add to that the fact that we have unprecedented monetary intervention, with interest rates no longer working and the Fed resorting to quantitative easing. We have massive fiscal deficits as far as the eye can see adding to the already burgeoning national debt. All of which calls into question how much wiggle room the government will have after the current suite of programs.

At the end of the day though, no one can truly claim to "know" with any degree of certainty which view is correct.

However, we can consider the pay-offs of different courses of action.

- If the government intervenes massively, and the "everything is normal" camp is right, then we will, at the the end, land up with an overheated economy and sharply rising taxes and interest rates at the other end which could stunt the pace of growth for over a decade. On the other hand, it would expedite recovery in the short run and potentially improve infrastructure in a way which wouldn't have happened without the intervention.

- If the government intervenes massively, and the "the sky is falling" camp is right, then we avoid a acalamity and recover from this recession in a way that makes it look like a just a slightly deeper version of a normal recession.

- If the government doesn't intervene, and the "everything is normal" camp is right, then we just have a slightly deeper recession but we come out of it structurally more sound and we would see slightly higher long term growth due to lower long term taxes and interest rates.

- If the government does nothing, and the "the sky is falling" is right, then the US and the world could experience a long depression, unemployment could rise to 20%+, and we would almost undoubtedly see massive wars and widespread famines. The end result could be a severe dent to the US domination of the world. Even otherwise, deep recessions have often been followed by periods of war, and we may yet see another one.

The more interesting thing is that Obama has opted for a middle road. As Paul Krugman (who is firmly in the "sky is falling" camp) explains, the current stimulus doesn't do much to plug the $2.9 trillion gap in the GDP projected by the CBO. For the roughly $600BN that will actually injected into the economy as part of the current stimulus package to actually be effective in plugging this gap, you need to assume that the velocity of money will be retained at current levels, i.e. it assumes that savings rates won't rise by too much. If you look at depressions, then that seems like a ridiculously optimistic presumption.

So, Obama is hedging his bets. This seems like a lose-lose proposition to me. If the "sky is falling" camp is right, then this won't be enough. If the "everything is normal" camp is right, it'll be too much. Net net, this will neither guarantee a rescue nor guarantee that we avoid the ills of overspending. Now, Obama may believe that the truth lies in the center and that a cautious incremental approach is better. And he may well be right. But he is banking on being able to get more legislation through Congress if and when the need arises. Let's hope he is right!

Thursday, February 12, 2009

The stimulus bill

Whew, so we have a stimulus bill, and Obama has discovered why so few have governed from the center. He has managed to dissatisfy everyone - the lefties are upset about the giveaways to the wealthy, the righties are upset about the huge spending. Anyway, here's what they are proposing:

Aggregate spending proposal totaling $311 BN, to be allocated as follows:

Aggregate spending proposal totaling $311 BN, to be allocated as follows:

- Investments in Infrastructure and Science - $120 billion

- Investments in Health - $14.2 billion

- Investments in Education and Training - $105.9 billion

- Investments in Energy, including over $30 billion in infrastructure - $37.5 billion

- Helping Americans Hit Hardest by the Economic Crisis - $24.3 billion

- Law Enforcement, Oversight, Other Programs - $7.8 billion

Let's put this in perspective. According the Federal budget estimates, the aggregate outlay by the US government projected for 2009 was $3.107 BN. This spending represents about a 10% increase in the US budget, or roughly 2% of the US GDP. This is through spending alone. While the exact numbers are hard to come by, new agencies are reporting on TV that almost 80% of this amount is likely to be spent in the next 18 months.

Meanwhile, there is a lot of discussion about the remaining part of the stimulus, reportedly $477 BN, a large part of which is in tax cuts. Haven't found the details on the web yet. Will post it when I do.

Is this package big enough? Probably not. At last not big enough to be sure it will work. But, if enough people start feeling good enough, it would stall the downward slide, and that might be a good start.

Friday, February 6, 2009

Putting things in perspective

This article puts some of the issues into perspective. This chart compares the job loss trend in this recession with the trend in the last two US recessions. Horrific!

Wednesday, January 28, 2009

US economy bad. Others worse.

While currently the economic woes in the US seem to be worse than in the EU, the IMF predicts that among developed nations, UK will be the worst hit with a contraction of 2.8% in 2009. The EU overall will shrink by 2%. The US will shrink by a "mere" 1.6% - that's roughly $220 BN reduction in the US GDP. Moreover, the IMF has warned that the UK is so structurally unsound that it will remain in debt for 20 years.

Of course, all this pales in comparison to Iceland. Iceland has become the first Western nation to get IMF help since 1976. With 17.1% inflation and outstanding bank debt that is six times its GDP, Iceland is expected to see 9.6% contraction in its GDP in 2009 and at best no growth in 2010. Their Prime Minister has now been forced to resign. Here's a summary of the timeline of key events in Iceland.

Meanwhile, while many developing economies have been ravaged by a combination of the drop in demand from Western economies and the drop in oil prices (a mixed blessing, depending on where you are), they are expected to continue to grow, although their growth will slow substantially.

Of course, all this pales in comparison to Iceland. Iceland has become the first Western nation to get IMF help since 1976. With 17.1% inflation and outstanding bank debt that is six times its GDP, Iceland is expected to see 9.6% contraction in its GDP in 2009 and at best no growth in 2010. Their Prime Minister has now been forced to resign. Here's a summary of the timeline of key events in Iceland.

Meanwhile, while many developing economies have been ravaged by a combination of the drop in demand from Western economies and the drop in oil prices (a mixed blessing, depending on where you are), they are expected to continue to grow, although their growth will slow substantially.

Where is all that money going?

I have been hearing about the profligate spending that is the Reinvestment and Reconstruction proposal more popularly called the "economic stimulus plan". So, I decided to investigate what they are proposing.

Here's the marked up summary of the proposal from the House Appropriations Committee, and of the tax portion from the house Ways and Means Committee. Obviously, this will change by the time of its passing.

The bad news, for people earning over $75K ($150K for married couples filing jointly), there is very little relief. Let's see if Obama lives up to his campaign promise of lowering taxes for everyone with income under $250K. It all depends on how they phase the relief out.

Here are some highlights of what they are proposing (I have highlighted in blue, those provisions that individuals earning more than $75K per capita would benefit from):

Here's the marked up summary of the proposal from the House Appropriations Committee, and of the tax portion from the house Ways and Means Committee. Obviously, this will change by the time of its passing.

The bad news, for people earning over $75K ($150K for married couples filing jointly), there is very little relief. Let's see if Obama lives up to his campaign promise of lowering taxes for everyone with income under $250K. It all depends on how they phase the relief out.

Here are some highlights of what they are proposing (I have highlighted in blue, those provisions that individuals earning more than $75K per capita would benefit from):

Taxation (these dollar amounts represent the cost over 10 years):

- $145 BN on a tax credit of 6.2% of earned income phasing out for people earning over $75K ($150K for married couples filing jointly);

- $4.60 BN on increase in earned income tax credits for very poor families;

- $18 BN on increasing child credit;

- $13 BN for college education assistance;

- $2.56 BN for assistance to first time home buyers;

- $27 BN for small businesses and acquiring companies;

- $50 BN for local and state government assistance;

- $16 BN on renewable energy investments;

- $4.27 BN on upto 30% tax credit capped to $1500 per annum on energy efficient improvements to existing homes, e.g. heaters, air conditioners, etc.

- $54 BN on cleaner and more efficient energy (there is a small amount set aside to subsidize energy star appliances);

- $16 BN on science, technology and Internet access;

- $90 BN on improving roads, bridges and waterways;

- $141.6 BN on improving educational facilities and educational programs for poor and under privileged;

- $24.1 BN on improving healthcare services - particularly their computer systems;

- $102 BN in unemployment and hunger prevention benefits;

- $91 BN in preventing lay-offs in the public sector - state and local governments;

A few things to note:

First, the $800 BN number being thrown around is misleading. The cost of the tax proposals is over 10 years. The summary released by the Appropriation Committee on the spending proposals don't explicitly state how these costs will be phased. MSNBC suggested on Hardball that a substantial portion of it will not get spent till Obama's second term.

If we assume that the tax benefits would more or less be uniform over the 10 years or even skewed a little to later years, assuming economic growth and that 80% of the spending would be over the next one or three years, this would mean that the actual impact over the next two years of the stimulus is probably more like: $450 BN - $550 BN. Worse, over $100 BN is actually just preventing cut backs in government spending. So, it isn't incremental spend. The incremental spend is more like, $350 BN - $450 BN. Worse, this is spread over two to three years, which means that the immediate impact is likely $150 BN to $200 BN, which is just about 1.5% of GDP. Given the expected contraction in GDP is 1.6%, this seems low to spur growth. It'll just about cover the gap.

In terms of who gets the benefit, if you ignore timing differences, here's the allocation:

Tax cuts for individuals: 20%

Education: 19%

State and local governments: 18%

Underprivileged: 13%

Basic infrastructure: 11%

Renewable energy: 9%

Small businesses: 3%

Healthcare: 3%

Science and technology: 2%

Unfortunately, most individuals won't see most of these benefits for a while yet, whereas the spending increases will take near immediate effect.

Monday, January 26, 2009

On the economic recovery plan etc.

For those who are struggling with history of recession solutions ranging from Supply Side economics to Keynesian economics, this is an excellent brief map of the history of recession management in the US since the 1960s. Kennedy was actually the first President to consciously try a Keynesian solution to a recession. The other President to use it extensively was Reagan (in effect, although not in intent).

I don't know about you, but I am increasingly exasperated by the certitude with which talking heads on TV make assertions reiterating partisan rhetoric on the "economic rescue plan". Why do experts of all hues insist on peddling opinions as fact, despite the complete lack of evidence? Why not reproduce the facts in an intelligible way and leave it for viewers to decide? The truth is they don't know the answers, despite their protestations to the contrary.

Here's Warren Buffet on the topic of the economy. I've reproduced one part of the interview for you below:

I don't know about you, but I am increasingly exasperated by the certitude with which talking heads on TV make assertions reiterating partisan rhetoric on the "economic rescue plan". Why do experts of all hues insist on peddling opinions as fact, despite the complete lack of evidence? Why not reproduce the facts in an intelligible way and leave it for viewers to decide? The truth is they don't know the answers, despite their protestations to the contrary.

Here's Warren Buffet on the topic of the economy. I've reproduced one part of the interview for you below:

Q: "... But there is debate about whether there should be fiscal stimulus, whether tax cuts work or not. There is all of this academic debate among economists. What do you think? Is that the right way to go with stimulus and tax cuts?"

Warren Buffet: "The answer is nobody knows. The economists don’t know. All you know is you throw everything at it and whether it’s more effective if you’re fighting a fire to be concentrating the water flow on this part or that part. You’re going to use every weapon you have in fighting it. And people, they do not know exactly what the effects are. Economists like to talk about it, but in the end they’ve been very, very wrong and most of them in recent years on this. We don’t know the perfect answers on it. What we do know is to stand by and do nothing is a terrible mistake or to follow Hoover-like policies would be a mistake and we don’t know how effective in the short run we don’t know how effective this will be and how quickly things will right themselves. We do know over time the American machine works wonderfully and it will work wonderfully again."

Couldn't agree with him more.

On a different note, the complexity of the economic woes has been excellently summarized by Samuelson in his Op-ed piece. As Samuelson astutely points out, the US is facing three separate economic crises:

- A decline in consumer spending. Consumer spending is 70% of the US economy. With the wiping off of over $7 trillion in personal wealth, people just aren't spending any more.

- A breakdown of the financial system. Financial institutions just aren't lending, and without credit, there is little chance of growth. Part of this has to do with ravaged balance sheets due to mounting losses - the target of the TARP. Part of this has to do with the loss in confidence in several market making derivative and other financial instruments. And, a major part has to do with the uncertainties around people and companies' income potential and the consequential difficulty in developing appropriate lending criteria.

- Slowdown in the rest of the world: This is no longer just a US crisis. The rest of the world is slowing down. While a much smaller part of the US economy, the slowdown in the rest of the world could thwart attempts to kick start growth in the US.

Finally, let's clear up the confusion between the New Deal and Keynesian economics.

Although, Maynard Keynes did advise FDR he was neither the primary advisor to FDR nor the architect of the New Deal. Keynes inter alia advocated massive deficit spending and government intervention to ensure full employment as a means of reversing the depression. As this brief history of the New Deal in Wikipedia suggests, FDR didn't exactly do that. In fact, the US was very conservative in its approach and even tried to return to balanced budgets in the mid-1930s, with disastrous consequences. It is true that many of the structures that regulate today's economy were set up or restructured during the New Deal. However, as an example of Keynesian economics, the New Deal provides at best mixed data that can be sampled to buttress claims by both sides of the argument. The equivalence of the New Deal with Keynesian economics therefore is somewhat misguided.

Saturday, December 27, 2008

Fear of cliffs

If you expected an article about the white cliffs of Dover, you will be sorely disappointed. I am referring here to cliff events in the context of the economy.

In recent days there have been frantic efforts by many in the government egged on by many reputed economists including advocates of free markets to intervene in the market and prop up failing institutions. They have intervened, but seemingly to little effect. What's going on? Why is there such a panic?

Underlying the theory of free markets is an assumption that free markets, even when not perfectly efficient, are mean reverting. This is why advocates of non-intervention speak of "market correction". The idea is that while there can be a distortion in value for a time, ultimately everything will automatically revert to a true value. Of course, this view assumes the existence of such am invariant 'true value'.

There is, however, a more interesting set of theories that have been evolving that postulate that natural systems, including financial markets are chaotic. This means, that while they may occasionally appear to be mean reverting, there is no reason that they should revert to a mean. Instead, even small changes can have extremely magnified effects resulting in a different level in the long run. In such systems, small changes can have huge, often catastrophic effects. Examples of such chaotic changes are literally the straw that breaks the camel's back or the butterfly effect. In this view, there are times when a financial system like the economy can stand at a brink, where on one side, it seems unwell but curable, and on the other it faces complete ruin.

Let me illustrate with an example.

In the early part of this decade, as Enron devolved into a financial debacle, disclosures made to ratings agencies put the ratings agencies in a quandary. On the one hand, if they continued to maintain the same credit rating, then it was possible that in the interim time the company could find a way to pull itself out of the mess. On the other hand, if they reduced the rating, then it would automatically trigger a series of obligations that would hinder Enron's ability to borrow. The resulting mess would lead to further downgrades, and so on, quickly reducing Enron to junk bond status.

This was an example of a credit cliff. It's a situation where a small change in the conditions, i.e. Enron's credit rating, could push it over a cliff.

Two things to note.

The problem is that the US economy as a whole is over-leveraged and over valued. The US need a HUGE amount of money to dig itself out. The only way for the US to get that money is that everyone continues to believe in the US.

With huge foreign holdings of US debt and US investments, if people suddenly started to doubt the US and started to disinvest, then the US economy could, in theory, collapse. The problem is that unlike the mean reverting view, in this view, the new equilibrium would leave the faith in the US economy so damaged that it would permanently destroy the US economy's value, and the US would never completely recover.

The Fed's experiment with Lehman caused a crash that has everyone spooked. They won't try it again. No other large US brand name can be allowed to fail. What the US government, Fed and all those illustrious economists are hoping is that if they can just hold on long enough, things will get better. They are banking on the assumption that it's in no one's interest to let the US fail. The alternative is a complete collapse of the US economy.

Are we really at such a cliff? Who knows? But you don't really want to find out by stepping off the ledge, do you?

However, note that all these interventions maintain a fiction. They keep you on the right side of the ledge. They don;t get you further away from the ledge. In fact, in some ways, they lift you up a bit, making the fall, if it comes, all the worse. So long as there is no catastrophic collapse of the economy, you could say these measures are working. But you are still at the edge.

To fix things, we still need to fix the underlying problem - asset price inflation. There are only two solutions. Either let the asset prices deflate. Or, let them stagnate until the value increases to the price. Neither is attractive. Both take time, maybe years. And, remember the second lesson from Enron is that ultimately the fiction can only maintained for so long. Let's hope the creditors of the US economy are more patient.

In recent days there have been frantic efforts by many in the government egged on by many reputed economists including advocates of free markets to intervene in the market and prop up failing institutions. They have intervened, but seemingly to little effect. What's going on? Why is there such a panic?

Underlying the theory of free markets is an assumption that free markets, even when not perfectly efficient, are mean reverting. This is why advocates of non-intervention speak of "market correction". The idea is that while there can be a distortion in value for a time, ultimately everything will automatically revert to a true value. Of course, this view assumes the existence of such am invariant 'true value'.

There is, however, a more interesting set of theories that have been evolving that postulate that natural systems, including financial markets are chaotic. This means, that while they may occasionally appear to be mean reverting, there is no reason that they should revert to a mean. Instead, even small changes can have extremely magnified effects resulting in a different level in the long run. In such systems, small changes can have huge, often catastrophic effects. Examples of such chaotic changes are literally the straw that breaks the camel's back or the butterfly effect. In this view, there are times when a financial system like the economy can stand at a brink, where on one side, it seems unwell but curable, and on the other it faces complete ruin.

Let me illustrate with an example.

In the early part of this decade, as Enron devolved into a financial debacle, disclosures made to ratings agencies put the ratings agencies in a quandary. On the one hand, if they continued to maintain the same credit rating, then it was possible that in the interim time the company could find a way to pull itself out of the mess. On the other hand, if they reduced the rating, then it would automatically trigger a series of obligations that would hinder Enron's ability to borrow. The resulting mess would lead to further downgrades, and so on, quickly reducing Enron to junk bond status.

This was an example of a credit cliff. It's a situation where a small change in the conditions, i.e. Enron's credit rating, could push it over a cliff.

Two things to note.

- Firstly, the cliff was characterized by the value was driven belief that was ultimately self referential - i.e. it had value because people believed it had value. It was solvent as long as people believed that it was and would continue to be solvent.

- Secondly, the fiction was ultimately unsustainable.

The problem is that the US economy as a whole is over-leveraged and over valued. The US need a HUGE amount of money to dig itself out. The only way for the US to get that money is that everyone continues to believe in the US.

With huge foreign holdings of US debt and US investments, if people suddenly started to doubt the US and started to disinvest, then the US economy could, in theory, collapse. The problem is that unlike the mean reverting view, in this view, the new equilibrium would leave the faith in the US economy so damaged that it would permanently destroy the US economy's value, and the US would never completely recover.

The Fed's experiment with Lehman caused a crash that has everyone spooked. They won't try it again. No other large US brand name can be allowed to fail. What the US government, Fed and all those illustrious economists are hoping is that if they can just hold on long enough, things will get better. They are banking on the assumption that it's in no one's interest to let the US fail. The alternative is a complete collapse of the US economy.

Are we really at such a cliff? Who knows? But you don't really want to find out by stepping off the ledge, do you?

However, note that all these interventions maintain a fiction. They keep you on the right side of the ledge. They don;t get you further away from the ledge. In fact, in some ways, they lift you up a bit, making the fall, if it comes, all the worse. So long as there is no catastrophic collapse of the economy, you could say these measures are working. But you are still at the edge.

To fix things, we still need to fix the underlying problem - asset price inflation. There are only two solutions. Either let the asset prices deflate. Or, let them stagnate until the value increases to the price. Neither is attractive. Both take time, maybe years. And, remember the second lesson from Enron is that ultimately the fiction can only maintained for so long. Let's hope the creditors of the US economy are more patient.

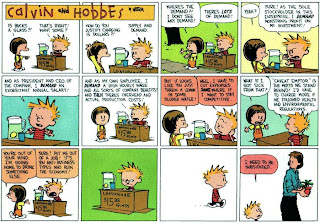

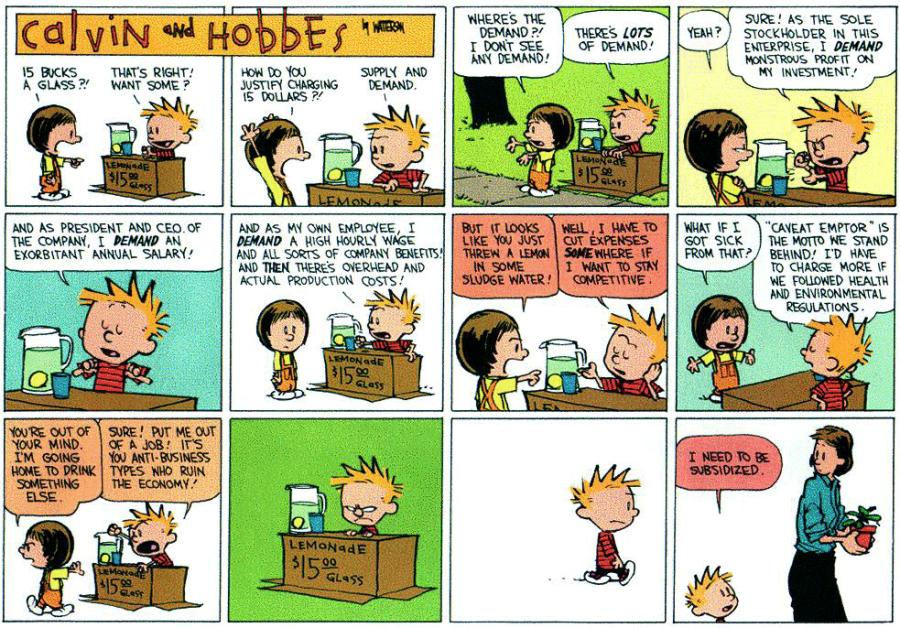

On the bailouts ...

Dhakks and I were having a discussion recently on the bailouts, and I was almost inspired to write a lengthy piece explaining my views. But then I came across this Calvin and Hobbes strip that does it so much better. Enjoy! (click on the strip to expand)

{kind=link}

Monday, December 1, 2008

Uncomfortable facts

In this article, Asra Nomani criticizes the conditions of Muslims in India and points out that this is a disaster waiting to happen. While it may be tempting to dismiss criticism of the Indian government policy towards Muslims as being ill conceived and insensitive, coming as it does just after a horrific terrorist attack, the data on this is pretty damning. Over the last twenty years (i.e. roughly since the mid-1980s), Muslims have fallen behind even the scheduled castes and tribes in terms of socio-economic progress. This report as part of the Sachhar Committee report shows some of this data. At minimum, this shows that while India is progressing, for one reason or the other, Muslims in India are being left behind. For the Muslim community to fall off so dramatically, there really has to be widespread disengagement. This is particularly evidenced by the fact that unlike Dalits and other minorities, and despite being the largest minority in India, there is no effective political advocacy on behalf of Muslims in the political process. This is not to validate the demands of Muslims, but more to highlight the lack of effective democratic outlet for Muslims.

This is a great article by Fareed Zarkaria where he, among other things, points out that these issues need to be resolved not just by India but by the whole region, as the problems bleed from one country to another.

One of the readers comments in the Fareed Zarkaria article alleges that the Indian Army and R&AW routinely engineer these incidents within India and then blame Pakistan. Searches for reports on the Sabarmati Express, Godhra incident, Malegaon blasts, etc. reveals a pot pourri of allegations of this kind emanating from news organizations from Pakistan and India. As with all news, people selectively remember the reports that supports their view of the world.

The underlying problem for people like the commenter though is that there is no credible trustworthy impartial arbiter of truth in the sub-continent. Even in horrific cases such as the Godhra incident, there are contrary opinions issued by different commissions. These commissions are often designed to make political hay out of lamentable situations, and as a result, people are left with doubts. Even to this day the facts in most of these cases are unclear.

Adding to confusion are the often wild and baseless accusations and claims made by the Indian media and politicians, which never get rescinded and are then absorbed into the ongoing memes in the Indian consciousness. How many terrorists were there in the latest attacks? How did they get there? Where are they from? All sorts of facts and speculation have been bandied about.

Some of these are harmless. But often, these factoids, despite being blatently false, feed and justify the views of extremists.

This is a great article by Fareed Zarkaria where he, among other things, points out that these issues need to be resolved not just by India but by the whole region, as the problems bleed from one country to another.

One of the readers comments in the Fareed Zarkaria article alleges that the Indian Army and R&AW routinely engineer these incidents within India and then blame Pakistan. Searches for reports on the Sabarmati Express, Godhra incident, Malegaon blasts, etc. reveals a pot pourri of allegations of this kind emanating from news organizations from Pakistan and India. As with all news, people selectively remember the reports that supports their view of the world.

The underlying problem for people like the commenter though is that there is no credible trustworthy impartial arbiter of truth in the sub-continent. Even in horrific cases such as the Godhra incident, there are contrary opinions issued by different commissions. These commissions are often designed to make political hay out of lamentable situations, and as a result, people are left with doubts. Even to this day the facts in most of these cases are unclear.

Adding to confusion are the often wild and baseless accusations and claims made by the Indian media and politicians, which never get rescinded and are then absorbed into the ongoing memes in the Indian consciousness. How many terrorists were there in the latest attacks? How did they get there? Where are they from? All sorts of facts and speculation have been bandied about.

Some of these are harmless. But often, these factoids, despite being blatently false, feed and justify the views of extremists.

Saturday, October 18, 2008

The sky is falling!

Volcker, the former Fed Chief says the US is in recession. Reactions to the recession forecasts have been strong. Gloom abounds. People are running around panicking like chickens. Conservatives are making gloomy predictions about how this will play out. In a recent article on the economy, David Brooks makes one such attempts at soothsaying. He predicts that Obama will ride this tide to a liberal overreach which will be followed by a conservative backlash. Very plausible.

Meanwhile, another interesting philosophical debate wages between liberals and conservatives, about whose view of the economy is right.

The liberals are crying vociferously that this means the end of free markets and the GOP approach to economics. They say it proves the GOP theories failed.

Meanwhile, the Libertarian fiscal conservatives are shouting that Bush is leading America to socialism, as illustrated this article on Ron Paul's economic adviser railing against Bush's socialism.

In a recent article on CNN, Jeffrey Miron, makes his case for free marketers, and waxes eloquently on why bankruptcy not bailout is the answer. Essentially, he points out that the bailout will reward the worst excesses and thereby facilitate the return of such excesses. By letting banks fail, you ensure that the system self corrects itself to a state where everyone is more prudent. You won't get good behavior, if you bail out the offenders every time they slip up. He also suggests that efforts to intervene will either distort the market or fail completely. On the whole, he advises doing nothing.

Others though are less sanguine. George Soros and others are pointing out that the free market system assumes that markets are self correcting. However, Soros suggests that the evidence is that markets are not. That to be self correcting they need regulations that ensure that the players play by the rules.

Others like Sloan point out that what is happening is just normal market correction and the cries of socialism or calls for re-examination of the whole structure of government are premature and unwarranted.

Meanwhile, Nassim Taleb is challenging one of the fundamental tenets of derivative pricing and thinks their Nobel prize should be revoked. Taleb's explanation is that the formula used by Merton, Black and Scholes was a widely known formula for Markov chains, and they merely applied it to economics. Further, he points out that the data shows that the Black Scholes approach is fundamentally wrong, as it assumes the distribution of rate changes is normally distributed, when in fact, the data shows that there is a significantly higher probability of extreme events than predicted by Black-Scholes.

So, which view is right? From a Scientific perspective, all the theories have merit. For instance, Supply-side and Keynesian economics both work. There is mountains of evidence that both do. There is mountains of evidence that blind adherence to one or the other doesn't. In the Asian crisis in the mid 1990s, Malaysia and Thailand went in opposite directions, and the results for their economies was much the same. So, net net, the economic theories seem a wash.

The reason of course has to do with the fact that these debates fail to realize two essential elements of economic theory. The first is that while economic theory can help frame up the debate about what could happen if you did A vs. B, it says nothing about which is better. What would happen is a scientific question and amenable to testing, whether it is good is a moral question and a choice.

For instance, raising taxes indefinitely would in fact reduce growth. However, not providing services like social security, defense, basic infrastructure, etc. for the economy, could be devastating for many people. So, taxes are necessary, too much is not. There is of course a trade-off. How much is good? The answer is how important is protecting people, providing healthcare etc. vs. making lots of money? By the way, it can be shown that at a certain point, the infrastructure will fail to the point that incremental tax breaks will no longer generate growth, but will retard growth.

The choice therefore is a moral one.

In a pure free market system, the length of the recession can be very long and the interim downward spiral would punish a lot of market participants. The people hardest hit would be those at the fringes, i.e. the poor and the middle class. If things were allowed to play out, ultimately it might correct, but not before wreaking devastation on huge numbers of people. The reason pure free market economics has never been applied in full is that whenever things get bad, the usually powerless populace reacts badly, voting out or throwing out the government and demanding change. The longer free market approaches are tried in bad times, the more political instability it creates.

Supply side economics works too. It enriches richer people first and prioritizing the plight of poor people lower. Ultimately everyone benefits. Given the incentive to rich, means that powerful market participants invest heavily, driving investment and growth. However, in general, while the benefits do trickle down, in most economies that have tried this, income disparities have grown, not shrunk. Ultimately, what that means is that poor people have substantially lower risk tolerance and richer people (i.e. people who drive the economy) have substantially higher. Ultimately, when the people in power can no longer empathise with people who are not, it can lead to very stupid risks - i.e. bubbles.\

Keynesian theories work too. The problem with them is that the allocation of money by the government is almost always a political decision and not an economic decision. Also, governments are notoriously bad at cutting back in good times. The effect of the two is that Keynesian intervention often creates huge market imbalances, lower productivity, higher structural unemployment (usually because giveaways reduce the incentive for people to go and find work), and significantly greater long term inflationary risk - because of government's inability to cut back. On the other hand Keynesian approach substantially reduces the impact on poor and middle class, and minimizes the risk for them.

Properly regulated and governed, in all three you can avoid the worst excesses.

These are no where near complete analysis. However, the larger point is that we need to choose what effect is desirable and choose the best tools to achieve it. No amount of examination of the tools can reveal the ideal goal.

This brings us to the second fallacy. As Soros points out, all human systems are flawed. And every decision has a measure of good and a measure of not so good. The good and the not so good can be concentrated on particular sections of the economy or spread around. Over time, the dogmatic continuation of any philosophy will create sufficient accretion of the not so good aspects where the good of that policy no longer offsets it. At that point, you need a different solution.

This brings me back to David Brooks' article. In the article, David Brooks describes the effect of an Obama government, and predicts that it will ultimately result in the revival of conservatism. It's not very clear whether he wants to pass judgment, but there is just a hint that conservatism in its purest form is the better philosophy. However, in describing the effect, Brooks has explained something else very eloquently - that governments in democracies are also market participants. The swing from liberalism to conservatism in a sense is the attempt by the market to find a balance between the evils of competing approaches. The longer we double down on one or the other philosophy, the more the imbalance it creates, and the more the need for a change in direction. So, what Brooks, describes a market place where the competing ideas seek balance and equilibrium. In this sense, democracy is enabling the free market to help drive the moral choices we make.

Friday, September 5, 2008

A stutter in India ...

Recently, there has been much talk about how India is going to become dominant in the world. This report on the issues facing Tata Nano production in West Bengal is an example of why that growth will not be easy. Quick summary, strikes and protests have stopped the construction of the Nano production facility in West Bengal.

Knowing West Bengal, they would have protested the construction no matter how much cause they had. A gut reaction would be to blame the intransigence of undereducated farmers, the hold of the communists and pandering by politicians. However, a closer look reveals that it may not be as simple as that. Government heavy handedness and a willingness by Indian companies to use government influence to strong arm people and not be fair were also to blame.

In this case, the West Bengal government literally took away hundreds of acres of farmland to give to the Tatas and paid the farmers "adequate compensation". Since there was no auction, the compensation is the government's estimate of the land's value, and not the market value it might have fetched. So, financially, its unclear how fair the deal is.

Also, imagine being a farmer and then having the only thing you know how to do being taken away from you, without your consent. It would be like someone giving me a packet of money and saying you can never work in a company again.

The Chinese by contrast do this relatively easily, for example in the relocation of 2 MM people during the construction of the 3 Gorges Dam. The question is, should India emulate the Chinese? Are the pains of the few less relevant than the gains of the many?

Knowing West Bengal, they would have protested the construction no matter how much cause they had. A gut reaction would be to blame the intransigence of undereducated farmers, the hold of the communists and pandering by politicians. However, a closer look reveals that it may not be as simple as that. Government heavy handedness and a willingness by Indian companies to use government influence to strong arm people and not be fair were also to blame.

In this case, the West Bengal government literally took away hundreds of acres of farmland to give to the Tatas and paid the farmers "adequate compensation". Since there was no auction, the compensation is the government's estimate of the land's value, and not the market value it might have fetched. So, financially, its unclear how fair the deal is.

Also, imagine being a farmer and then having the only thing you know how to do being taken away from you, without your consent. It would be like someone giving me a packet of money and saying you can never work in a company again.

The Chinese by contrast do this relatively easily, for example in the relocation of 2 MM people during the construction of the 3 Gorges Dam. The question is, should India emulate the Chinese? Are the pains of the few less relevant than the gains of the many?

Subscribe to:

Posts (Atom)